Revenue Can Create a False Sense of Success

Revenue Can Create a False Sense of Success

A vacation rental may generate strong bookings, high occupancy and impressive gross revenue while producing little profit. This happens when managers focus on sales but fail to measure the full cost of earning them.

Gross revenue is the total income generated before deductions. It may include accommodation revenue, cleaning fees, extra services, cancellation income and other guest charges. Profit is what remains after commissions, operating costs and structural expenses.

For owners, confusing revenue with profit can create unrealistic expectations. For property managers, it can hide weak margins, underpriced services and properties that consume more resources than they contribute.

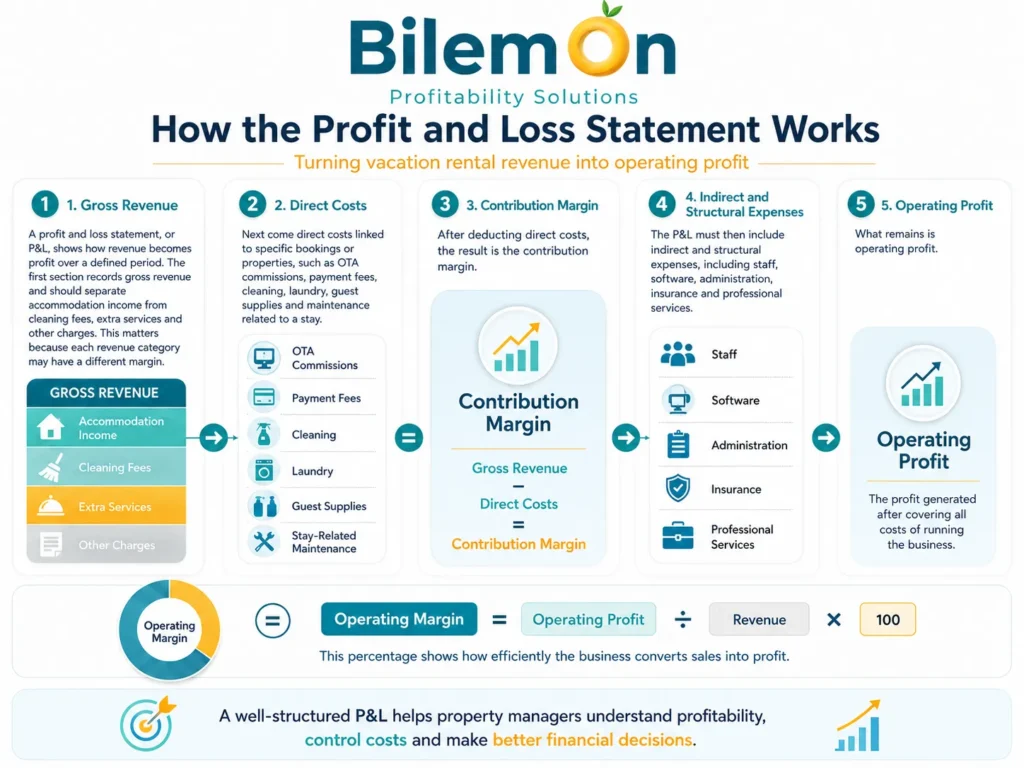

How the Profit and Loss Statement Works

A profit and loss statement, or P&L, shows how revenue becomes profit over a defined period.

The first section records gross revenue and should separate accommodation income from cleaning fees, extra services and other charges. This matters because each revenue category may have a different margin.

Next come direct costs linked to specific bookings or properties, such as OTA commissions, payment fees, cleaning, laundry, guest supplies and maintenance related to a stay.

After deducting direct costs, the result is the contribution margin. The P&L must then include indirect and structural expenses, including staff, software, administration, insurance and professional services. What remains is operating profit.

Operating Margin = Operating Profit ÷ Revenue × 100

This percentage shows how efficiently the business converts sales into profit.

Operating Margin = Operating Profit ÷ Revenue × 100

how can we help you?

Contact us at the Consulting WP office nearest to you or submit a business inquiry online.

Looking for Clearer Profitability Control?

A Simplified Example

Consider a property generating €10,000 in monthly gross revenue:

Accommodation revenue: €9,000

Cleaning fees: €800

Additional services: €200

Direct costs:

OTA commissions: €1,350

Cleaning and laundry: €1,200

Guest supplies and minor maintenance: €450

Contribution after direct costs: €7,000

Allocated operating expenses:

Management staff and guest support: €1,500

Software and administration: €500

Property-related overhead: €600

Operating profit: €4,400

The property generated €10,000 in gross revenue, but only €4,400 in operating profit. Its operating margin was 44%.

This example is simplified, but it shows why revenue should never be treated as profit. Cash must also be reviewed separately. Revenue may appear in the P&L before the OTA transfers the money to the bank.

Common Mistakes

One mistake is ignoring OTA commissions because platforms deduct them before payment. This hides the true distribution cost.

Another is failing to assign costs to the correct property. When cleaning, maintenance or support expenses remain at portfolio level, profitable and unprofitable units become difficult to identify.

A third mistake is mixing owner funds with management company revenue. Money collected on behalf of an owner is not automatically income for the manager.

PMS reports should also be reconciled with OTA statements, invoices, owner settlements and bank transactions.

Better Decisions Through Accurate Data

A reliable P&L helps managers adjust prices, review OTA dependence, renegotiate owner agreements, control supplier costs and identify properties that fail to produce an acceptable margin.

It also improves budgeting, cash flow planning and owner reporting. Bilemon centralizes booking, property, owner, revenue, cost, PMS and bank data, helping managers measure profitability by property and across the portfolio.

Conclusion

Accounting is not only a reporting obligation. A well-structured P&L shows where revenue comes from, where money is spent and which properties truly create value.

Property managers who understand the difference between gross revenue, cash and profit can protect margins, improve financial visibility and make better business decisions.